ACCOUNTS OCTOBER 2016 BOARD PAPER

Book Keeping & Accountancy July 2016 Board Paper

July 2016 Board Paper

(1) What is Trial Balance?

Ans. Trial balance is a statement showing the list debit and credit balances of all the ledger accounts on a particular date.

(2) What shows credit balance of revaluation account?

Ans. Profit on Revaluation Account.

(3) What are ‘convertible debentures’?

Ans. Convertible Debentures; - Convertible Debentures are those which can be converted either partly or wholly into equity shares after the completion of a definite period. The rate of interest and date of conversion is decided at the time of issue. The interest is paid up to the date of conversion. On conversion the debenture holders are eligible for dividends and other rights and privileges of shareholders.

(4) Who is ‘Payee’?

Ans. Payee is the person or party to whom the amount of bill is made payable.

(5) What is single entry system?

Ans. A bookkeeping system that only records one aspect of each business transaction. i.e. either debit or credit is called single entry system.

ACCOUNTS BOARD PAPERS

- Accounts - March 2025 - English Medium Download Answer Key

- Accounts - March 2025 - Marathi Medium Download Answer Key

- Accounts - March 2025 - Hindi Medium Download Answer Key

- Accounts - July 2025 - English Medium Download Answer Key

- Accounts - March 2024 English Medium Download Answer Key

- Accounts - March 2024 - Marathi Medium Download Answer Key

- Accounts - March 2024 - Hindi Medium Download Answer Key

- Accounts - July 2024 - English Medium Download Answer Key

- Accounts - July 2023 - English Medium Download Answer Key

- Accounts - March 2022 View

- Accounts - July 2022 Download Answer Key

- Accounts - March 2021 Download Answer Key

- Accounts - March 2020 View

- Accounts - March 2014 View

- Accounts - October 2014 View

- Accounts - March 2015 View

- Accounts - July 2015 View

- Accounts - March 2016 View

- Accounts - July 2016 Viewhttps://www.omtexclasses.com/2017/12/accounts-october-2016-board-paper.html

- Accounts - July 2017 View

- Accounts - March 2017 View

- Accounts - March 2018 View

- Accounts - July 2018 View

- Accounts - March 2019 View

(1) The accounts which are prepared at the end of each financial year.

Ans. Trading and Profit and Loss Account.

(2) The fees paid by a person who wants to become a life member of the concern, for his whole life.

Ans. Life membership fees.

(3) The acknowledgement of debt under common seal of company.

Ans. Debenture Certificate

(4) Payment of the bill before its due date.

Ans. Retirement of Bill.

(5) Critical evaluation of financial statement to measure profitability.

Ans. Analysis of financial statement

(1) All indirect expenses are debited to ____________ account.

(a) Trading

(b) Capital

(c) Profit and Loss

(d) Current

(2) Share of profit of a deceased partner till the date of death is ____________

(a) debited to profit and loss adjustment account.

(b) credited to profit and loss adjustment account.

(c) debited to profit and loss suspense account.

(d) credited to profit and loss suspense account.

(3) If any asset is taken over by a partner from the firm, his capital account will be ______________

(a) credited

(b) debited

(c) added

(d) none of these

(4) There are ____________ parties to the Bill of Exchange.

(a) two

(b) three

(c) four

(d) five

(5) Further capital introduced during the year is _________ from closing capital in order to find out the correct profit.

(a) added

(b) deducted

(c) divided

(d) ignored

(1) All receipts are the items of revenue income. [False]

(2) At the time of dissolution loan from partner will be transferred to realisation account. [False]

(3) A Bill of Exchange is a negotiable instrument. [True]

(4) Acceptance without making any change in the terms of bill is called general acceptance. [True]

(5) Ratio analysis is useful for inter - firm comparison. [True]

Shri Arjun Patil, 104, Shivaji Nagar, Ambajogai draws a two months bill on Shri Tukaram Magdum, Daulat Road, Halkarni, Kolhapur payable to Shri Ranveer Patil, Mondha, Parali Vaijanath on 23 rd August, 2013 for Rs. 7550. Shri Tukaram Magdum accepted it on 28th August, 2013 for Rs. 7500 only.

Answer:

| Particulars | 1.4.2012 Amount (Rs. ) |

31.3.2013 Amount (Rs.) |

|---|---|---|

| Investments | 12000 | |

| Bank overdraft | 10000 | |

| Bills payable | 5000 | 8000 |

| Creditors | 26500 | 31500 |

| Furniture | 9000 | 19000 |

| Debtors | 35000 | 50000 |

| Stock | 15000 | 19000 |

| Bank Balance | 18000 | 28000 |

Further information:

- Mrs. Shailaja withdrew Rs. 4000 for her personal use. She received Rs. 15,000 from her father as gift, which she brought into the business.

- Additional furniture was purchased on 01.10.2012. Depreciate furniture by 10% p.a.

- Write off Rs. 1,000 as bad debts and provide 5% R.D.D. on debtors.

Prepare: Opening and closing statement of affairs and statement of profit or loss for the year ended 31st March, 2013.

Click Here for Answers(A) Explain the limitations of analysis of financial statements.

Click Here for Answer(B) Explain the operating activities on cash flow.

Click Here for AnswerBalance Sheet as on 31st March, 2010

| Liabilities | Amt. | Amt. | Assets | Amt. | Amt. |

|---|---|---|---|---|---|

| Creditors | 38000 | Cash in Hand | 37000 | ||

| Bills Payable | 46000 | Stock | 21000 | ||

| Profit & Loss A/c | 16000 | Debtors | 46000 | ||

| Capital A/c | (-) R.D.D. | -6000 | 40000 | ||

| Harish | 100000 | Equipments | 12000 | ||

| Girish | 140000 | 240000 | Furniture | 25000 | |

| Plant | 85000 | ||||

| 340000 | Buildings | 120000 | |||

| 340000 |

They admitted Shirish on 1st April, 2010 on the following conditions:

- For his 1/3 rd share in the future profits, Shirish brings Rs. 2,00,000 as his capital.

- It is decided to raise goodwill by Rs. 90,000 and write off fully after Shirish Admission.

- Equipments and Plant are to be depreciated by 20% and 10 % respectively and Building is to be appreciated by 15%.

- Bills Payable were retired for Rs. 35,000.

- All debtors are to be considered good.

- Furniture of the book value Rs. 12,000 was taken over by Harish at 40% of the book value.

Prepare, Revaluation A/c. Partners' Capital A/c and Balance Sheet of the new firm.

Click Here for AnswerAnita, Sunita and Kavita were partners sharing profits and losses in the ratio 3:3:2. Their Balance Sheet as on 31st March 2013 is as below:

Balance Sheet as on 31st March, 2013.

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

|---|---|---|---|

| Capital Accounts | Building | 10000 | |

| Anita | 11000 | Machinery | 10700 |

| Sunita | 15000 | Furniture | 10000 |

| Kavita | 8000 | Debtors | 5000 |

| Creditors | 10000 | Stock | 6600 |

| Reserve fund | 4000 | Cash | 6600 |

| 48900 | 48900 |

On 1st April, 2013, Mrs. Kavita retired from the firm on the following terms:

- Goodwill of the firm is to be valued at Rs. 4,000, however, only Kavita’s share in it is to be raised in the books and written off immediately.

- Assets to be revalued as under:

Stock Rs. 6,300; Machinery Rs. 10,000; Furniture Rs. 10,200. - R.D.D. to be maintained at 10% on debtors.

- Rs. 100 to be written off from creditors.

- The amount payable to Mrs. Kavita is to be transferred to her loan account.

Prepare :

- Profit and loss adjustment account.

- Partner’s capital account, and

- Balance Sheet of new firm as on 01.04.2013.

(A) Arvind renews his acceptance of Jaydeep of ` 7,000 with interest ` 500 for two months.

(B) Bank informed Jaydeep that Mahadev’s acceptance of ` 4,000 which was discounted and dishonoured. Bank charged noting charges ` 80.

(C) Hanumant informed Jaydeep that Kazi’s acceptance for ` 7,000 endorsed to Hanumant has been dishonoured, noting charges `85.

(D) Datta honoured his acceptance of `4,900, which was sent to bank for collection. Bank debited ` 100 for bank charges.

(E) Radhika retired her acceptance to Jaydeep of ` 9,000 by paying ` 8,700.

Click Here For Journal EntriesBalance Sheet as on 31st Mar, 2013

| Liabilities | Amount (Rs. ) | Assets | Amount (Rs.) | Amount (Rs.) |

|---|---|---|---|---|

| Sundry Creditors | 20000 | Cash at Bank | 8000 | |

| Bills Payable | 5000 | Debtors | 16000 | |

| General Reserve | 6000 | Less: R.D.D. | -1000 | 15000 |

| Rahul’s Loan A/c | 16000 | Stock | 20000 | |

| Capital Account | Plant and Machinery | 30000 | ||

| Rahul | 25000 | Furniture | 6000 | |

| Rohit | 10000 | Ramesh’s Capital Account | 3000 | |

| 82000 | 82000 |

The firm was dissolved on the above date:

- Assets realised as follows:

Debtors Rs. 9,000, Plant and Machinery Rs. 26,000, Stock Rs. 14,000, and Furniture Rs. 3,000. - The creditors were paid Rs. 18,000, in full settlement and the bills payable were paid in full.

- The realisation expenses amounted to Rs. 3,000.

- Ramesh became insolvent and was able to bring in only Rs. 1,800 from his private estate.

Prepare:

- Realisation account

- Partner’s capital account and

- Bank account.

Journalise the transactions and also show Balance Sheet.

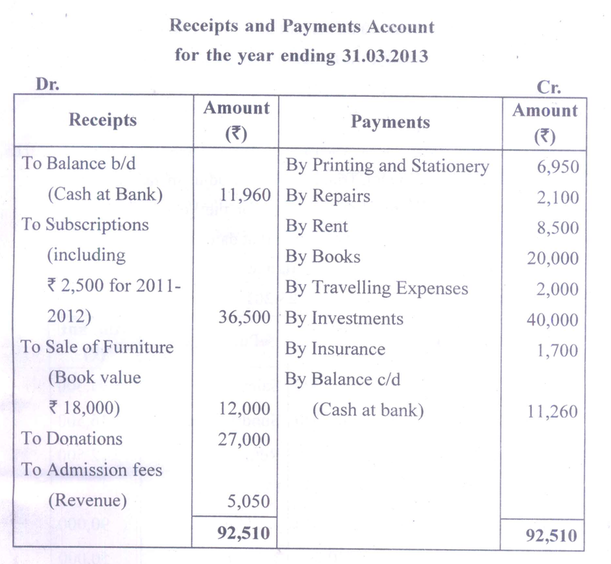

Receipts and Payment Account for the year ending 31.03.2013

| Receipts | Amount (Rs.) | Payments | Amount (Rs.) |

|---|---|---|---|

| To Balance b/d (Cash at Bank) | 11960 | By Printing & Stationery | 6950 |

| To Subscriptions (including Rs. 2,500 For 2011-2012) | 36,500 | By Repairs | 2,100 |

| To Sale of Furniture (Book value Rs. 18,000) | 12,000 | By Rent | 8,500 |

| To Donations | 27000 | By Books | 20000 |

| To Admission Fees (Revenue) | 5050 | By Travelling Expenses | 2000 |

| By Investments | 40000 | ||

| By Insurance | 1700 | ||

| By Balance c/d [Cash at Bank] | 11200 | ||

| 92510 | 92510 |

Additional Information:

| Particulars | 01.04.2012 Amount | 31.03.2013 Amount |

|---|---|---|

| Outstanding Subscriptions Furniture Building fund Capital fund Investments |

3,000 32,000 1,45,000 1,51,960 2,50,000 |

5,000 ? ? ? ? |

- Neglect depreciation on the part of furniture sold during the year, but depreciate the remaining furniture by Rs. 1,000.

- Donation is received for building fund.

Trial Balance as on 31.03.2013

| Particulars | Amount Rs. | Particulars | Amount Rs. |

|---|---|---|---|

| Opening Stock Purchases Plant and Machinery Furniture Carriage Wages Bills Receivable Sundry Debtors Conveyance Salaries Cash in hand Land and Building Bad debts Patents |

32,000 64,000 30,000 18,500 1,500 30,000 5,000 32,000 4,000 10,500 14,750 83,500 1,750 25,000 |

Sales Sundry Creditors Return Outward Capital Accounts’ Dhiraj Suraj |

1,93,500 16,500 2,500 90,000 50,000 |

| 352500 | 352500 |

Adjustments :

- Closing stock: Cost price RS. 25,000 and market price Rs. 30,000.

- An amount of Rs. 3,500 spent for repairs to building is debited to building account.

- Depreciate plant and machinery and building at 5% p.a.

- Included in wages in advance given to workers Rs. 3,000.

- Provide Rs. 1,500 for bad and doubtful debts on debtors.

Book-keeping and Accountancy 12th Standard HSC Maharashtra State Board. Latest Syllabus.

Chapter 1: Introduction to Partnership and Partnership Final Accounts

Chapter 2: Accounts of ‘Not for Profit’ Concerns

Chapter 3: Reconstitution of Partnership (Admission of Partner)

Chapter 4: Reconstitution of Partnership (Retirement of Partner)

Chapter 5: Reconstitution of Partnership (Death of Partner)

Chapter 6: Dissolution of Partnership Firm

Chapter 8: Company Accounts - Issue of Shares