HSC ACCOUNTS MARCH 2018 BOARD QUESTION PAPER

Q 1. A. Answer:

- Trial Balance is a list of all debit and credit balances of ledger accounts.

- Entrance fees is the fees paid by the person who intends to become members of ‘not for profit concern’.

- Qualified acceptance is a type of acceptance in which drawee makes changes in the conditions mentioned in the bill.

- Gain ratio is required to be calculated in case of retirement of partner, when goodwill is raised equal to share of retiring partner and written off.

-

Gross Profit Ratio =Gross Profit Net Sales× 100

Q 1. B. Answers:

- (1) Unrecorded assets

- (2) Capital

- (3) Endorsee

- (4) Gain ratio

- (5) Single Entry System

HSC Accounts Board Papers with Solution

- Accounts - March 2025 - English Medium Download Answer Key

- Accounts - March 2025 - Marathi Medium Download Answer Key

- Accounts - March 2025 - Hindi Medium Download Answer Key

- Accounts - July 2025 - English Medium Download Answer Key

- Accounts - March 2024 English Medium Download Answer Key

- Accounts - March 2024 - Marathi Medium Download Answer Key

- Accounts - March 2024 - Hindi Medium Download Answer Key

- Accounts - July 2024 - English Medium Download Answer Key

- Accounts - July 2023 - English Medium Download Answer Key

- Accounts - March 2022 View

- Accounts - July 2022 Download Answer Key

- Accounts - March 2021 Download Answer Key

- Accounts - March 2020 View

- Accounts - March 2014 View

- Accounts - October 2014 View

- Accounts - March 2015 View

- Accounts - July 2015 View

- Accounts - March 2016 View

- Accounts - July 2016 View

- Accounts - July 2017 View

- Accounts - March 2017 View

- Accounts - March 2018 View

- Accounts - July 2018 View

- Accounts - March 2019 View

Q 1. C. Answers:

- (1) Debited

- (2) 25th January, 2017

- (3) Statement of Affairs.

- (4) Realization Account.

- (5) Purchases.

Q 1. D. Answers.

- (1) False.

- (2) True

- (3) True

- (4) True

- (5) True

Q. 2. Single Entry Solution:

Q. 3. Admission of Partner Solution:

Q. 3. Death of a partner Solution:

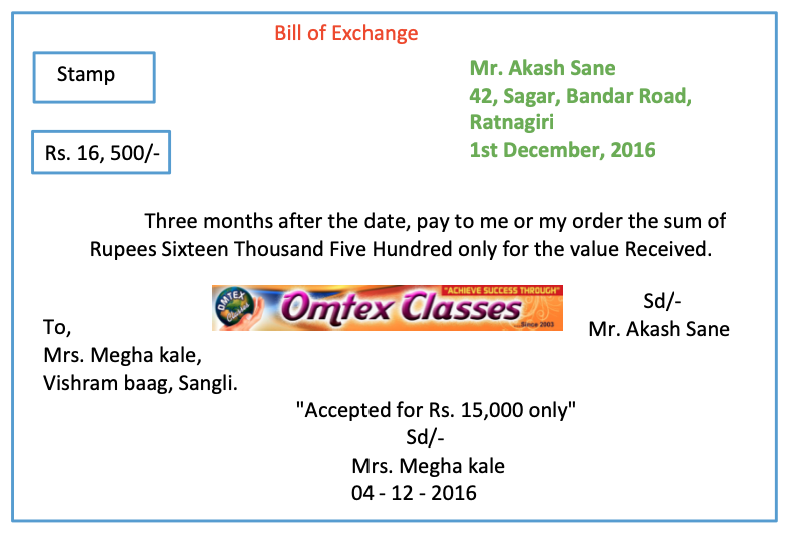

Q. 4. Bills of Exchange Solution:

Q. 5. Dissolution Solution:

OR

Q. 5. Issue of Equity Shares Solution:

Q. 6. NPO Solution:

Q. 7. FINAL ACCOUNT SOLUTION:

Book-keeping and Accountancy 12th Standard

HSC Maharashtra State Board. Latest Syllabus.

- Chapter 1: Introduction to Partnership and Partnership Final Accounts

- Chapter 2: Accounts of ‘Not for Profit’ Concerns

- Chapter 3: Reconstitution of Partnership (Admission of Partner)

- Chapter 4: Reconstitution of Partnership (Retirement of Partner)

- Chapter 5: Reconstitution of Partnership (Death of Partner)

- Chapter 6: Dissolution of Partnership Firm

- Chapter 7: Bills of Exchange

- Chapter 8: Company Accounts - Issue of Shares

- Chapter 9: Analysis of Financial Statements

- Chapter 10: Computer In Accounting

ACCOUNTS BOARD PAPERS

- HSC Accounts March 2020 Board Paper With Solution

- MARCH 2014 : View | PDF Download

- OCTOBER 2014 : View | PDF Download

- MARCH 2015 : View | PDF Download

- JULY 2015 : View | PDF Download

- MARCH 2016 : View | PDF Download

- JULY 2016 : View | PDF Download

- JULY 2017 : View | PDF Download

- MARCH 2017 : View | PDF Download

- MARCH 2018 : View | PDF Download

- JULY 2018 : View | PDF Download

- MARCH 2019 : View | PDF Download

- MARCH 2020 : View | PDF Download

Difficult Words & Meanings:

Trial Balance: A statement showing the balances of all ledger accounts to check arithmetic accuracy.

Ledger Accounts: The main book of accounts where transactions are recorded under specific headings.

Debit: An entry on the left side of an account, typically representing an increase in assets/expenses or a decrease in liability/equity/income.

Credit: An entry on the right side of an account, typically representing a decrease in assets/expenses or an increase in liability/equity/income.

Entrance Fees: A fee paid by new members to join an organization, especially a 'not-for-profit concern'.

Not for Profit Concern (NPO): An organization that operates for a social cause, not to make profit (e.g., charities, clubs).

Qualified Acceptance: When the drawee (person asked to pay a bill) agrees to pay but with some changes to the bill's original terms.

Drawee: The person or entity directed by a drawer (writer of the bill) to pay a specified sum of money on a bill of exchange.

Gain Ratio: A ratio used in partnership accounting, especially during a partner's retirement or death, to determine how remaining partners will share the outgoing partner's portion of profits or goodwill.

Goodwill: The intangible value of a business based on its reputation, customer base, etc., beyond its tangible assets.

Endorsee: The person to whom a bill of exchange or promissory note is transferred (endorsed).

Single Entry System: A simple bookkeeping method that records only cash and personal accounts, not using the double-entry principle.

Statement of Affairs: A summary of assets and liabilities, similar to a balance sheet, often prepared in single entry systems or insolvency cases.

Realization Account: An account prepared during the dissolution (closing down) of a partnership firm to record the sale of assets and payment of liabilities.

Reconstitution of Partnership: Any change in the existing agreement between partners, such as admission, retirement, or death of a partner.

Dissolution of Partnership Firm: The process of closing down a partnership business entirely.

Equity Shares: Shares that represent ownership in a company and give shareholders voting rights.

How closing stock became 70,000

ReplyDeletesame doubt

DeleteMarket prices =84000=20%

DeleteCost price = ???=100%

100×84000

------ = 70000

120

YEAH RIGHT

Delete84000x120÷100=70000

Delete84,000

Delete_______ × 100 =70,000

120

84000×100÷120 =70000 this is the correct solution of calculating closing stock

DeleteSame doubt

ReplyDelete100×84000/120

Delete=70000

84000×100

Delete______

120

Closing stock price is 20% higher than the original cost so 84000x120

Delete_____

100

Market price of ₹.84000 (20%) depricate

ReplyDelete100+20=120

84000×100÷12 = 70000 (closing stock)

Sorry its 84000 ×100÷120=70000

DeleteHow we got the amount of depreciation of machinery And what should we do of the second adjustment machinery??

ReplyDeleteMachinery is given 90000.But in adjustment it is given that machinery includes purchase of machinery for Rs.40000 on 1st January,2016.

DeleteSo,in the asset side you have to show,

Machinery=50000

(+) Purchase =40000

Therefore, 50000*10/100 + 40000*3/12*10/100.

Nice thx nice thanks

DeleteI didn't understood the machinery's Adjustment

ReplyDeleteMachinery adjustment mein kya diya hai Machinery include purachase of machinery for ₹40000 on 1st jan 2016.. jo new machinery purchase kiye the 1st jan ko woh machinery me include hua hai toh phir old machinery 50000 pe pure saal ka nikalenge aur new machinery 40000 pe 3 mahine ka nikalenge 1st jan 2016 ke hisaab se

DeleteSo jao fir

DeleteI didn't understood the salaries adjustment . How 3600 came?

ReplyDelete18000 10 month ka hai toh 2 mahina o/s hai 18000 ko 10 se divide karke ek mahine ka nikalke fir usko 2 mahine ka

Deletekardenge aaajayega 3600 o/s

Thank you ..for this adjustment... Its really helpful for us

DeleteSee first you depreciation on half yrr amount 50000into 10and divided by 100.than you get answers 5000

DeleteAnd second think is 40000into 3and divided by 12 than you get answers 1000 the total is 6000 fine

This comment has been removed by the author.

ReplyDeleteSir 5 adj. me machinery 40000 purchase se less hogi and asset me machinery add hogi ??

ReplyDeleteNhi.....5th adjustment mein kya diya machinery includes purchase of machinery for ₹40000 on 1jan 2016 .....machinery jo prchase kiye the 1stjan ko woh include ho chuki hai toh old machinery 50000 pe pure year ka depriciate karenge aur jo new machinery hai 40000 ki uspe 3 month ka depriciate karna hai

DeleteHai tho per

DeleteHow is goodwill calculated in the sum of admission

ReplyDelete144000/- Is a goodwill of total firm. The new partner is admitted for 1/4th share...so

Delete144000/4

=36000

36000/3 (Old partners ratio)

=12000/-

Thus, 12000×2= meena

12000/- heena

How the goodwill is calculated ?

ReplyDeleteWhat will be the 1st and 2nd effect in machinery aaj

ReplyDelete8%Debentureka effect kha hoga or kese calculated krege

ReplyDeleteSecond wala effect P and L A/c Main hoga

DeleteAur usse calculate main hame 8 % dentures main add karne hoge

You guys did the best work for us jai omtex classes

ReplyDeleteNice

DeleteHow is current account amount camed

ReplyDeleteIf current account is given then we have to directly write our capital balance to libality side and after it.after closing partner current account you have to write result value as current amount on libality side.

DeleteHow machinery became 6000???

ReplyDelete144000÷4=36000

ReplyDelete2-24000

1-12000

Joint ????

ReplyDeleteMCQ. 1ST ONE IS CRADIT

ReplyDeletehow come machinery deprication came 6000 it must 9000 and how to do 5 adjustment

ReplyDeleteclosing stock is 84000 as given , if 35% given what answer would be?

ReplyDeleteI am not understanding last adjustment

ReplyDeleteAgar telly nhi krenge toh kitna marks cut hoga ???

ReplyDelete1 or 2

DeleteHii sir

ReplyDeleteOne given answer plzz tell me

ReplyDeleteThanks i have solved without any of the solution there was calculations mistake which Nedd to come here

ReplyDeleteIn single entry ( depreciation on machinery on 30,000 for 6 months) what a answer and how calculate this ???

ReplyDelete