HSC ACCOUNTS MARCH 2018 BOARD QUESTION PAPER

Q 1. A. Answer:

- Trial Balance is a list of all debit and credit balances of ledger accounts.

- Entrance fees is the fees paid by the person who intends to become members of ‘not for profit concern’.

- Qualified acceptance is a type of acceptance in which drawee makes changes in the conditions mentioned in the bill.

- Gain ratio is required to be calculated in case of retirement of partner, when goodwill is raised equal to share of retiring partner and written off.

-

Q 1. B. Answers:

- (1) Unrecorded assets

- (2) Capital

- (3) Endorsee

- (4) Gain ratio

- (5) Single Entry System

Q 1. C. Answers:

- (1) Debited

- (2) 25th January, 2017

- (3) Statement of Affairs.

- (4) Realization Account.

- (5) Purchases.

Q 1. D. Answers.

- (1) False.

- (2) True

- (3) True

- (4) True

- (5) True

Q. 2. Single Entry Solution:

Q. 3. Admission of Partner Solution:

Q. 3. Death of a partner Solution:

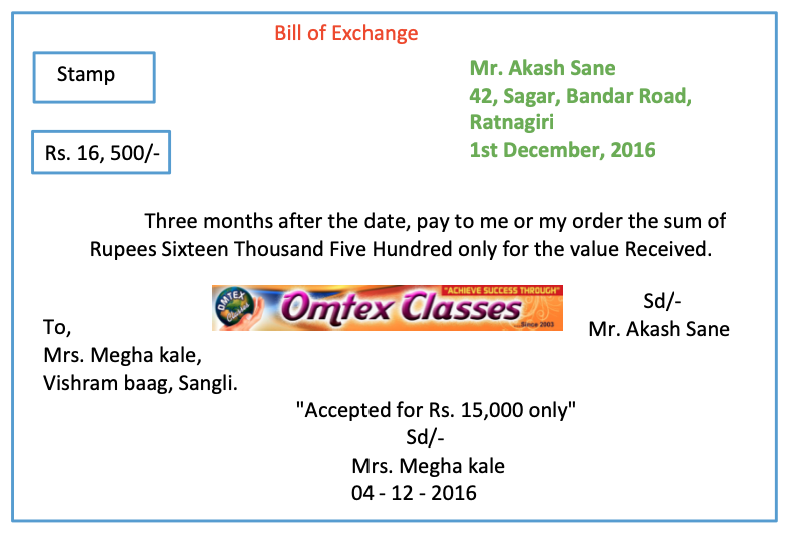

Q. 4. Bills of Exchange Solution:

Q. 5. Dissolution Solution:

OR

Q. 5. Issue of Equity Shares Solution:

Q. 6. NPO Solution:

Q. 7. FINAL ACCOUNT SOLUTION:

Book-keeping and Accountancy 12th Standard

HSC Maharashtra State Board. Latest Syllabus.

- Chapter 1: Introduction to Partnership and Partnership Final Accounts

- Chapter 2: Accounts of ‘Not for Profit’ Concerns

- Chapter 3: Reconstitution of Partnership (Admission of Partner)

- Chapter 4: Reconstitution of Partnership (Retirement of Partner)

- Chapter 5: Reconstitution of Partnership (Death of Partner)

- Chapter 6: Dissolution of Partnership Firm

- Chapter 7: Bills of Exchange

- Chapter 8: Company Accounts - Issue of Shares

- Chapter 9: Analysis of Financial Statements

- Chapter 10: Computer In Accounting

ACCOUNTS BOARD PAPERS

- HSC Accounts March 2020 Board Paper With Solution

- MARCH 2014 : View | PDF Download

- OCTOBER 2014 : View | PDF Download

- MARCH 2015 : View | PDF Download

- JULY 2015 : View | PDF Download

- MARCH 2016 : View | PDF Download

- JULY 2016 : View | PDF Download

- JULY 2017 : View | PDF Download

- MARCH 2017 : View | PDF Download

- MARCH 2018 : View | PDF Download

- JULY 2018 : View | PDF Download

- MARCH 2019 : View | PDF Download

- MARCH 2020 : View | PDF Download

Difficult Words & Meanings:

Trial Balance: A statement showing the balances of all ledger accounts to check arithmetic accuracy.

Ledger Accounts: The main book of accounts where transactions are recorded under specific headings.

Debit: An entry on the left side of an account, typically representing an increase in assets/expenses or a decrease in liability/equity/income.

Credit: An entry on the right side of an account, typically representing a decrease in assets/expenses or an increase in liability/equity/income.

Entrance Fees: A fee paid by new members to join an organization, especially a 'not-for-profit concern'.

Not for Profit Concern (NPO): An organization that operates for a social cause, not to make profit (e.g., charities, clubs).

Qualified Acceptance: When the drawee (person asked to pay a bill) agrees to pay but with some changes to the bill's original terms.

Drawee: The person or entity directed by a drawer (writer of the bill) to pay a specified sum of money on a bill of exchange.

Gain Ratio: A ratio used in partnership accounting, especially during a partner's retirement or death, to determine how remaining partners will share the outgoing partner's portion of profits or goodwill.

Goodwill: The intangible value of a business based on its reputation, customer base, etc., beyond its tangible assets.

Endorsee: The person to whom a bill of exchange or promissory note is transferred (endorsed).

Single Entry System: A simple bookkeeping method that records only cash and personal accounts, not using the double-entry principle.

Statement of Affairs: A summary of assets and liabilities, similar to a balance sheet, often prepared in single entry systems or insolvency cases.

Realization Account: An account prepared during the dissolution (closing down) of a partnership firm to record the sale of assets and payment of liabilities.

Reconstitution of Partnership: Any change in the existing agreement between partners, such as admission, retirement, or death of a partner.

Dissolution of Partnership Firm: The process of closing down a partnership business entirely.

Equity Shares: Shares that represent ownership in a company and give shareholders voting rights.