Single Entry Solution

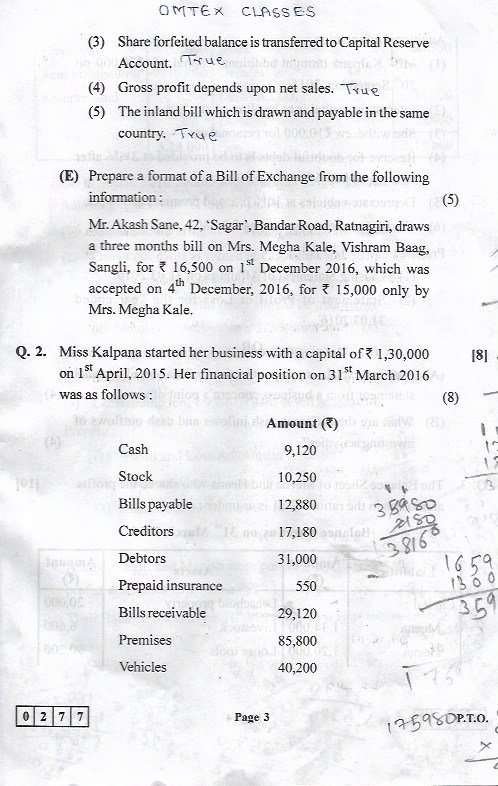

March 2018 HSC Board PaperIn the books of Miss Kalpana

Closing Statement of Affairs as on 31st March, 2016Swipe table left/right to view amounts →

| Liabilities | Amount | Assets | Amount |

|---|---|---|---|

| Bills payable | 12,880 | Cash | 9,120 |

| Creditors | 17,180 | Stock | 10,250 |

| Capital (Balancing Figure) | 1,75,980 | Debtors | 31,000 |

| Prepaid Insurance | 550 | ||

| Bills Receivable | 29,120 | ||

| Premises | 85,800 | ||

| Vehicles | 40,200 | ||

| Total | 2,06,040 | Total | 2,06,040 |

Statement of Profit or Loss

For the year ended 31st March, 2016Swipe table left/right to view amounts →

| Particulars | Amount (Rs.) | Amount (Rs.) |

|---|---|---|

| Capital at the end of the year. | 1,75,980 | |

| Add: Drawings during the year | 10,000 | |

| 1,85,980 | ||

| Less: Additional Capital Introduced | - 20,000 | |

| Adjusted Closing capital | 1,65,980 | |

| Less: Capital at the beginning of the year. | - 1,30,000 | |

| Profit Before Adjustments | 35,980 | |

| Add: Incomes and Gains during the year | ||

| Decrease in the value of creditors | 2,180 | |

| 38,160 | ||

| Less: Expenses and losses During the year. | ||

| (1) Interest on Capital (6500 + 500) | 7,000 | |

| (2) Bad debts | 1,000 | |

| (3) Reserve for Doubtful Debts | 750 | |

| (4) Depreciation on Vehicles | 4,020 | |

| (5) Depreciation on Premises | 4,290 | - 17,060 |

| NET PROFIT | 21,100 |

Thank you omtex classes You easy every thing

ReplyDeleteThanks a lot

ReplyDeleteThank u guys

ReplyDeleteThank you intex classes

ReplyDeleteIt's omtex ,

DeleteThank you omtex classes

ReplyDeleteTy omtex classes

ReplyDeleteThanks

ReplyDeleteCan i solve this sum in alternative method in board exam???

ReplyDeletePlz,reply as soon as possible...

no

DeleteThnx and dua ki guzarish hai

DeleteThank you Omtex classes

ReplyDeleteHow is interest on capital calculated

ReplyDelete5% on opening capital and 5% on additional capital for 6 months...

DeleteHow we are calculate capital please reply I do not understand

Delete130000×5÷100=6,500

DeleteOn additional capital we calculate the 5% interest I.e.20000×5÷100×6÷12=500

DeleteThanks for your help 😊👍😊

DeleteAdjustment overvalue and undervalue

ReplyDeleteEffects

We have to show working note or not?

ReplyDeleteYess

DeleteThank you omtex classes

ReplyDeleteHow to calculate intereste on capital?

ReplyDeleteSame question

Deletewhere is the class in pune

Deletewhere is the class in pune what ishe about fees

ReplyDeleteThank you

ReplyDeleteThank you

ReplyDeleteThank you

ReplyDeleteThank you

ReplyDeleteThanks sir🙂

ReplyDeletei dont like BK it is boring 😈 so single entry is boring

ReplyDeleteB.k it is not boring it is interesting 🧐🧐😁

ReplyDeleteWorking note is compulsory

ReplyDeleteNope

DeleteRDD is not a 750

ReplyDeleteRight answer is 775

No 750is correct ans because first of all we have to deduct 1000 from 31000 then we have to calculate 21/2% rdd on debtors i.e 750

Delete1500 will be the answer..

DeleteRdd is 750 because first we have to subtract (31000-1000)then charge 5% so we get 750 only

ReplyDelete750 or 1500??????

DeleteThanku 😘😘

DeleteThanks

ReplyDeleteThank u for halp me to this question

ReplyDeleteThank u

ReplyDeleteInterest on capital opening aur additional dono pe nikal ne ka?

ReplyDeleteThank You For Given Answer To Me and I have My Lot's Of Problem Sir In Book Keeping Accountncy

ReplyDeleteThanks sir

ReplyDeleteSir , net profit 1100 hai

ReplyDeleteOvervaluation of liabilities (i.e overvaluation of creditors) will be added and not subtracted... right?

ReplyDeleteThank you so much sir😊

ReplyDeleteWhat does creditors were overdraft mean? Please reply soon.

ReplyDelete